Insights & Resources

Financial planning perspectives for families, retirees, and business owners along 30A and nationwide.

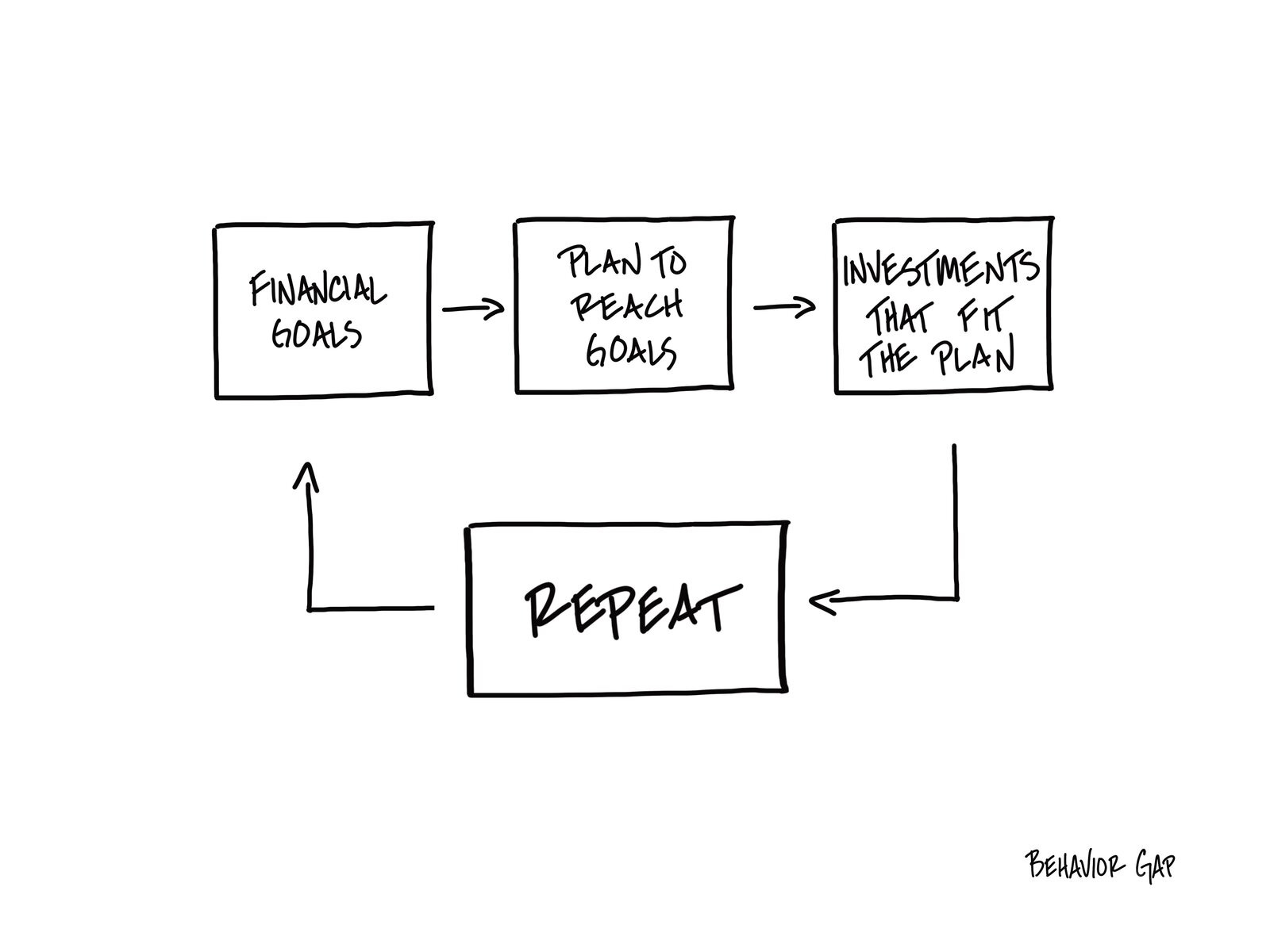

Planning Pillars

Financial planning perspectives for families, retirees, and business owners along 30A and nationwide.