In 2024, forecasters expected a manageable Atlantic hurricane season. The Pacific was not sending strong suppressive signals, and the season should have been unremarkable. Instead, the Atlantic produced 18 named storms, 11 hurricanes, and 5 major hurricanes. Hurricane Milton went from a tropical storm to a Category 5 in under 24 hours. Five hurricanes made U.S. landfall, making it the third-costliest season on record.

The families who absorbed that season best were not the ones who read the forecasts correctly. They were the ones whose insurance, liquidity, and property decisions did not depend on the forecast being right. That distinction matters more than most people realize, and the place to start understanding it is roughly 8,000 miles from the Florida coast, in the equatorial Pacific Ocean.

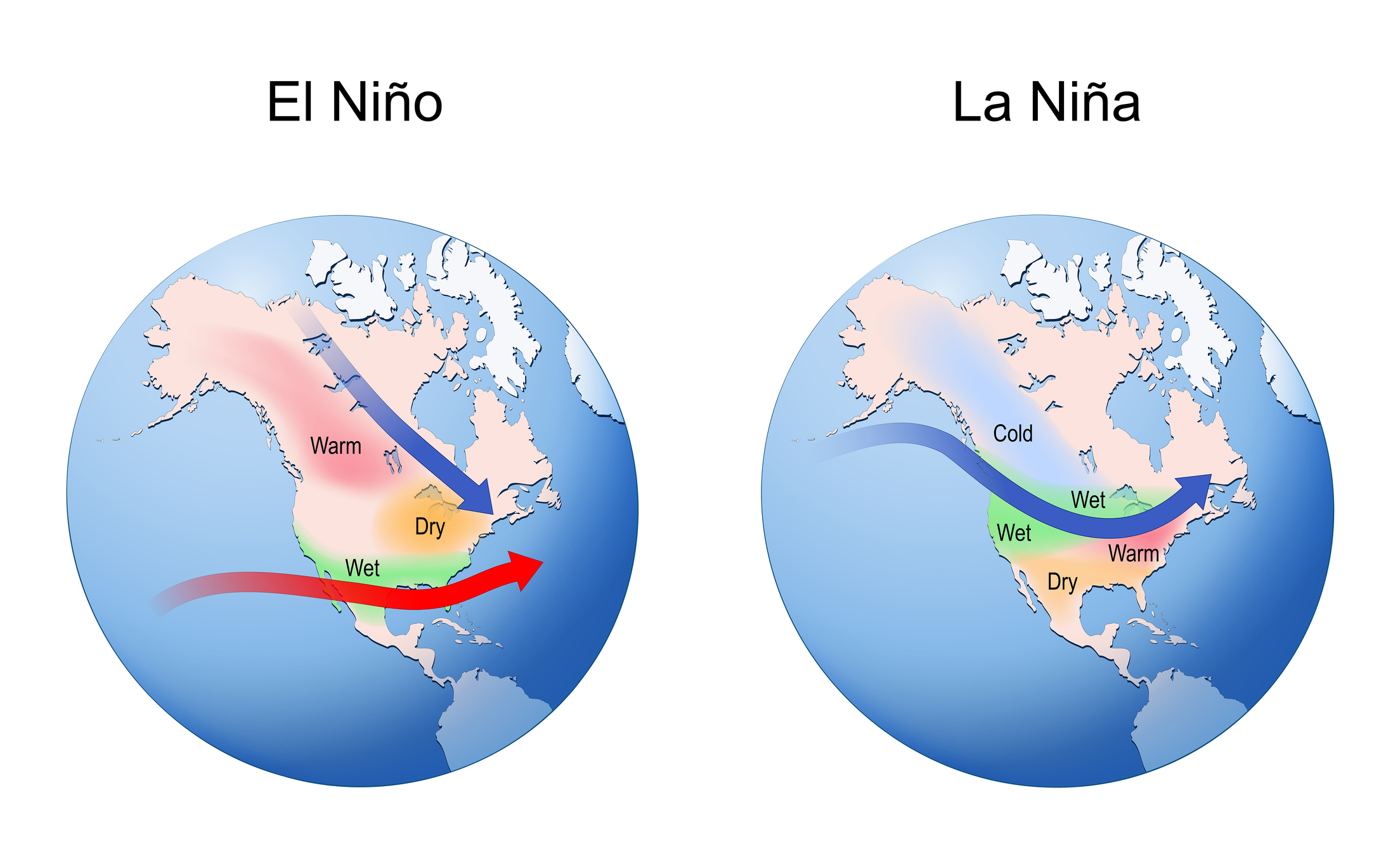

What ENSO Actually Is

ENSO, the El Niño-Southern Oscillation, describes a recurring pattern of ocean temperature changes in the central and eastern tropical Pacific. It cycles through three phases: El Niño (warmer-than-average Pacific surface temperatures), La Niña (cooler-than-average Pacific surface temperatures), and neutral. Each phase typically lasts around 9 to 12 months, though some persist longer, and the broader cycle repeats every 2 to 7 years.

These temperature shifts alter global atmospheric circulation, and the Atlantic hurricane basin is one of the regions most affected.

How El Niño Suppresses Atlantic Hurricanes

During El Niño, warmer Pacific waters strengthen upper-level westerly winds across the Atlantic basin, increasing vertical wind shear, the difference in wind speed and direction between the lower and upper atmosphere. Hurricanes need vertically aligned, stable conditions to form and strengthen. Wind shear disrupts that structure, often preventing storms from organizing.

Historically, El Niño years have produced materially fewer U.S. hurricane landfalls than neutral or La Niña years. A frequently cited NOAA analysis of 1900-1997 hurricane landfalls found the probability of two or more U.S. hurricane landfalls drops to about 28% during El Niño, compared to 48% during neutral years and 66% during La Niña. That is a meaningful shift in probabilities. It is not protection.

How La Niña Increases Risk

La Niña is the opposite pattern. Cooler Pacific waters weaken upper-level winds over the Atlantic, reducing wind shear and creating a more favorable environment for storm formation. At the same time, La Niña tends to coincide with warmer Atlantic sea surface temperatures and reduced atmospheric stability. The result is not just more storms, but more storms that intensify.

During La Niña years, the probability of at least one major hurricane making U.S. landfall rises significantly, and many of the most destructive recent seasons occurred under La Niña or transitioning conditions.

Why 2024 Did Not Behave the Way People Expected

If ENSO were the whole story, 2024 would have looked manageable. Instead, the Atlantic produced one of its most active and destructive seasons in the modern record. The reason is instructive.

ENSO conditions during the core of the season were largely neutral, not strongly suppressive. At the same time, Atlantic sea surface temperatures were at record or near-record levels. That thermal energy provided fuel that offset what would normally have been a less favorable atmospheric setup.

Storms like Milton did not just form. They intensified rapidly, with wind speeds increasing by more than 35 mph in under 24 hours, meeting the National Hurricane Center's formal definition of rapid intensification. The lesson is simple, but often misunderstood: ENSO is a predictor of tendency, not certainty. And this is where most planning mistakes begin.

The Behavioral Layer Most People Miss

Families do not misjudge hurricane risk because they are careless. They misjudge it because of how human judgment works. Kahneman and Tversky described this as the availability heuristic: we estimate probability based on how easily examples come to mind. After a major storm, risk feels higher than it statistically is. After a quiet period, it feels lower. Neither perception is reliable.

The FamilyVest approach is to recognize instinct, then build a plan that does not depend on it. We do not prepare for hurricanes based on memory. We prepare based on probabilities, balance sheets, and what would happen if the wrong scenario shows up at the wrong time. That is the difference between reacting to risk and managing it.

What Forecasters Are Saying About 2026

As of early 2026, NOAA's Climate Prediction Center projects a transition from La Niña to ENSO-neutral conditions in spring, with El Niño likely emerging by summer. Current models show roughly a 62% probability of El Niño during the June-August peak, rising to 72-80% through the end of the year.

Early-season forecast ranges from major outlets are consistent with that signal:

AccuWeather (March 2026): 11-16 named storms, 4-7 hurricanes, 2-4 major hurricanes.

Tropical Storm Risk (December 2025): 14 named storms, 7 hurricanes, 3 major hurricanes.

NOAA's official seasonal forecast, typically released in May, is not yet available at the time of writing.

That suggests a near-normal to slightly below-normal season. But "below normal" does not mean low risk. A single well-positioned Category 3 storm can cause more damage than an entire season of storms that never make landfall.

Geographic models also indicate elevated landfall probability along the northern Gulf Coast and parts of the Carolinas, directly relevant for families along the Emerald Coast.

What This Means for Your Financial Plan

Understanding ENSO does not change whether you need a hurricane plan. You do. What it changes is how you think about timing, preparation, and decision-making under uncertainty.

Insurance Coverage

Review your homeowner's, flood, and windstorm coverage well before the season begins. Most carriers impose binding restrictions once a credible storm threat emerges, and if you wait for the forecast to look concerning, you are often already too late.

Florida remains one of the most expensive insurance markets in the country. Average homeowner premiums now exceed $4,000 annually, with coastal properties often running $6,000 to $10,000 or more once flood and windstorm riders are layered in. Citizens Property Insurance, the state's insurer of last resort, cut rates 8.8% for 2026, but that reflects temporary claims improvement, not a structural shift in risk.

Equally important is carrier quality. Over a dozen regional insurers have gone insolvent in the past five years, and major national carriers have pulled back from high-risk zones. A lower premium from a carrier that folds during a claim is worse than no policy at all. For more on developing a comprehensive hurricane plan, see our guide on why Florida residents need a hurricane plan.

Emergency Liquidity

The standard recommendation is to set aside three to six months of living expenses in cash. For Florida homeowners, that baseline is incomplete. You also need to account for your hurricane deductible. In Florida, hurricane deductibles are calculated as a percentage of your dwelling coverage, with common options of 2%, 5%, or 10% of the insured value.

On a $1.5 million home, a 2% deductible means $30,000 out of pocket before coverage applies. At 5%, that is $75,000. If you cannot absorb that without selling investments under pressure, your liquidity plan is not aligned with your actual risk.

Property Decisions

ENSO is a short-term signal. Property ownership is a long-term commitment. The more important trends are structural: Atlantic sea surface temperatures are rising, rapid intensification events are becoming more common, and insurance costs are increasing while becoming less predictable. These are not one-year variables. They are 10-20-year forces.

For relocating families, this is part of the cost analysis that often gets underestimated. The relocation calculator on our site includes insurance cost comparisons, but those are averages. Your specific property's elevation, construction year, roof type, and proximity to water will drive your actual premium. Get real quotes before committing to a purchase.

When evaluating a coastal purchase, insurance should not be treated as a static expense. It should be modeled as a growing cost with potential availability constraints.

The Rapid Intensification Problem

Rapid intensification, defined by the National Hurricane Center as a wind speed increase of at least 35 mph within 24 hours, is the scenario that compresses decision timelines the most.

Recent research published in Geophysical Research Letters (2025) found that ENSO modulates not just overall storm counts but also the rate at which storms rapidly intensify. In a warmer Atlantic, even El Niño years may not reliably suppress the most dangerous rapid-intensification events as historical data would suggest.

This is where planning discipline matters. The real risk is not the average season. It is the scenario in which a storm strengthens quickly, shifts track late, and forces simultaneous decisions on evacuation, liquidity, and claims.

The Bottom Line

El Niño years tend to produce fewer Atlantic hurricanes. La Niña years tend to produce more. The 2026 season is likely to develop under El Niño conditions, which historically reduces activity, but "reduced" is relative. The Atlantic is warmer than it used to be, storm behavior is changing, and the relationship between ENSO and outcomes is becoming less predictable at the margins.

The correct response is not to adjust your level of concern. It is to standardize your level of preparation. Review your coverage. Verify your liquidity. Do both before June. ENSO is context. It is not a strategy.

If you want help evaluating how hurricane exposure fits into your broader financial plan, including insurance adequacy, emergency reserves, and risk management strategies for your family, start a conversation.