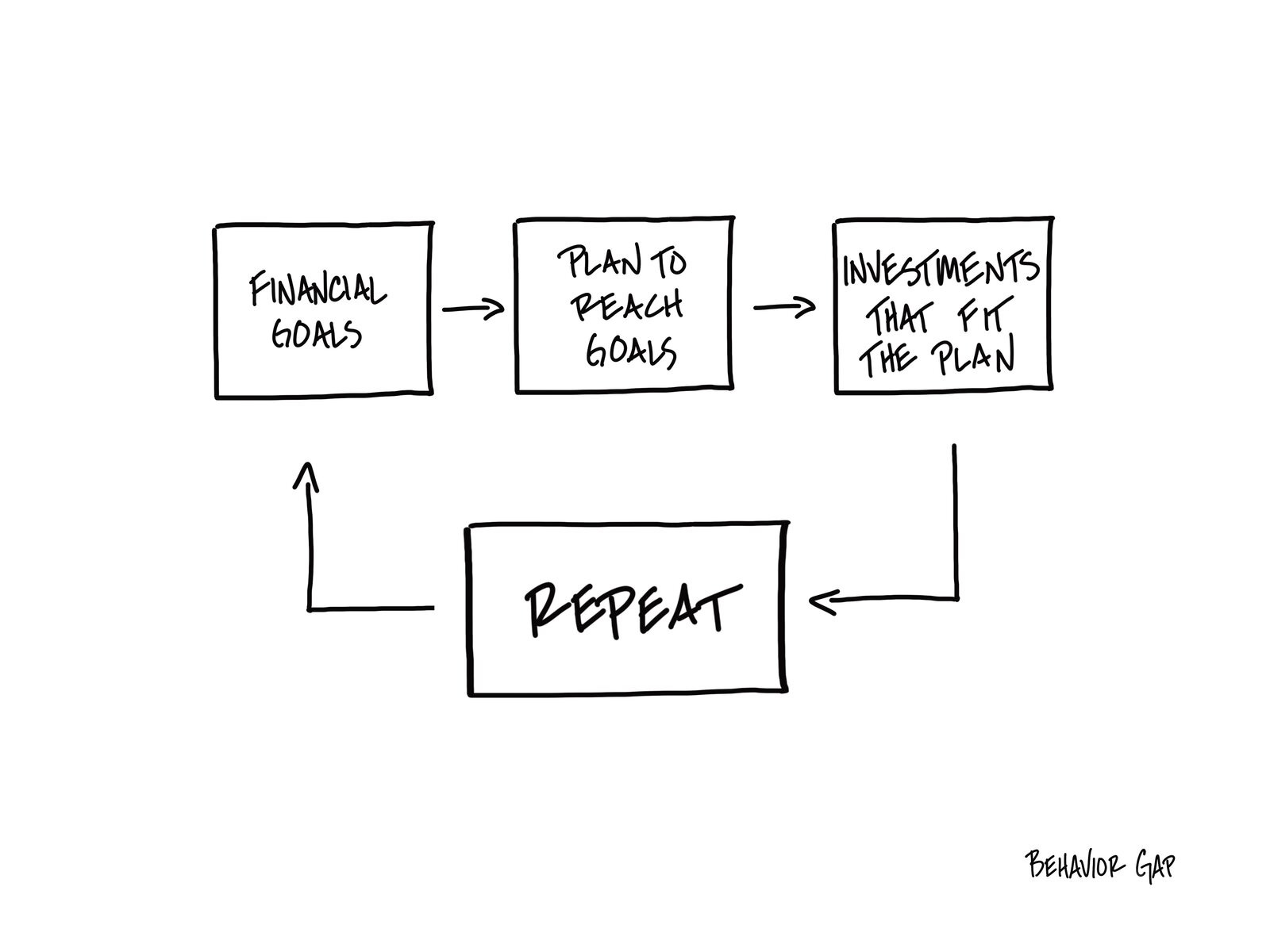

The order is not arbitrary.

Most financial advisors lead with investment management because that is where the fee is clearest. We lead with goals and planning because an investment portfolio that isn't connected to a plan is just a collection of positions.

The sequence - listen, plan, deliver, manage - ensures that every financial decision we make is traceable back to something you told us you wanted. When the market drops, your portfolio doesn't panic because it was never built on market optimism. It was built on your goals, with a plan designed to absorb volatility without requiring you to change your life.

That is what comprehensive financial planning means. Not a financial plan as a document, but planning as a discipline: ongoing, coordinated across every area of your financial life, and accountable to the goals you set at the beginning. Retirement, taxes, estate strategy, insurance, and investments are not separate conversations. They are one conversation, and we manage them that way.